Download the full document here.

Commenting on the new vehicle sales statistics for the month of January 2019, Naamsa said domestic new vehicle sales had started the year on a weak note principally due to “lower than expected” new car sales.

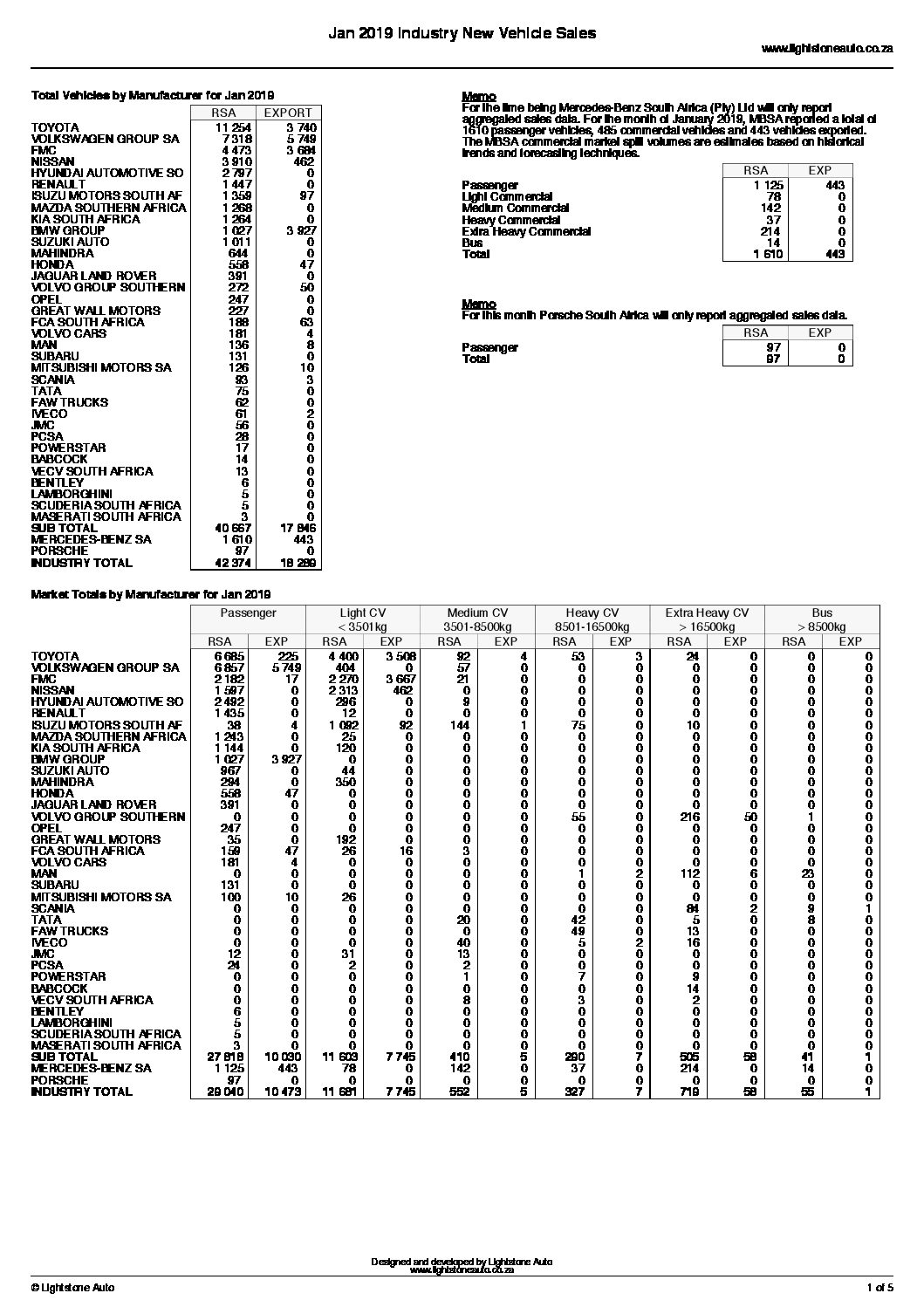

In the event, aggregate domestic sales at 42 374 units had declined by 3 398 units or 7,4 percent from the 45 772 vehicles sold in January last year. In contrast, export sales had started the year on a relatively strong note with January 2019 export sales at 18 289 vehicles, reflecting a substantial improvement of 4 160 vehicles or a gain of 29,4 percent compared with the 14 129 vehicles exported in January 2018.

South Africa had experienced a low growth environment over the past five years and it was generally expected that this would continue until after the general election, Naamsa said. Hopefully, post-election policy reforms and government’s commitment to revitalise the South African economy with the aim of achieving a substantially higher economic growth rate should translate into improved domestic sales numbers during the second half of 2019, the association added.

Overall, out of the total reported industry sales of 42 374 vehicles, an estimated 33 633 units or 79,4 percent represented dealer sales, an estimated 14,3 percent represented sales to the vehicle rental industry, 3,5 percent to government and 2,8 percent to industry corporate fleets.

The January 2019 new car market had been particularly weak and at 29 040 had registered a fall of 3 512 cars or a decline of 10,8 percent compared with the 32 552 new cars sold in January last year. As had been the case for most of 2018, the car rental industry had made a major contribution accounting for 19,9 percent of new car sales in January 2019 – translating into one in every five new cars sold during the month being a car rental sale.

Domestic sales of new light commercial vehicles, bakkies and mini buses at 11 681 units during January 2019 was virtually unchanged from the 11 679 light commercial vehicles sold during the corresponding month last year.

Sales in the low-volume medium and heavy truck segments had held up relatively well and at 552 units and 1 101 units, respectively, reflected a gain of 109 vehicles or an improvement of 24,6 percent in the case of medium commercial vehicles, and, in the case of heavy trucks and buses, a marginal improvement of three vehicles or a gain of 0,3 percent compared with the corresponding month last year.

The January 2019 export sales number was encouraging in view of the fact that a major vehicle exporter had only restarted production at the end of January 2019 to allow for plant refurbishment. Despite this, January 2019 export sales at 18 289 vehicles showed a substantial improvement of 4 160 units or a gain of 29,4 percent compared with the 14 129 vehicles exported in the same month last year. The momentum of vehicle exports over the course of 2019 was expected to increase substantially and industry export sales for the year were, at this stage, projected at around 385 000 units compared to the 351 139 vehicles exported last year.

Prospects for domestic new vehicle sales would be affected by the subdued current macro-economic environment and pressure on consumers’ disposable income, Naamsa said. The November 2018 0,25 percent increase in interest rates had impacted on new car demand due to higher vehicle financing costs.

Most automotive companies expected new vehicle sales to be flat during the first half of the year, however, following the general election and policy reforms, including expectations of a growth enhancing budget, domestic sales should improve during the second half of the year. The expected business conditions component of the latest Purchasing Managers’ Index, which tracked expected business conditions in six months time, had risen sharply.

Besides this positive development, average new vehicle pricing remained at around 2,5 percent remained well below the inflation rate and this would assist in improved new vehicle affordability for consumers.