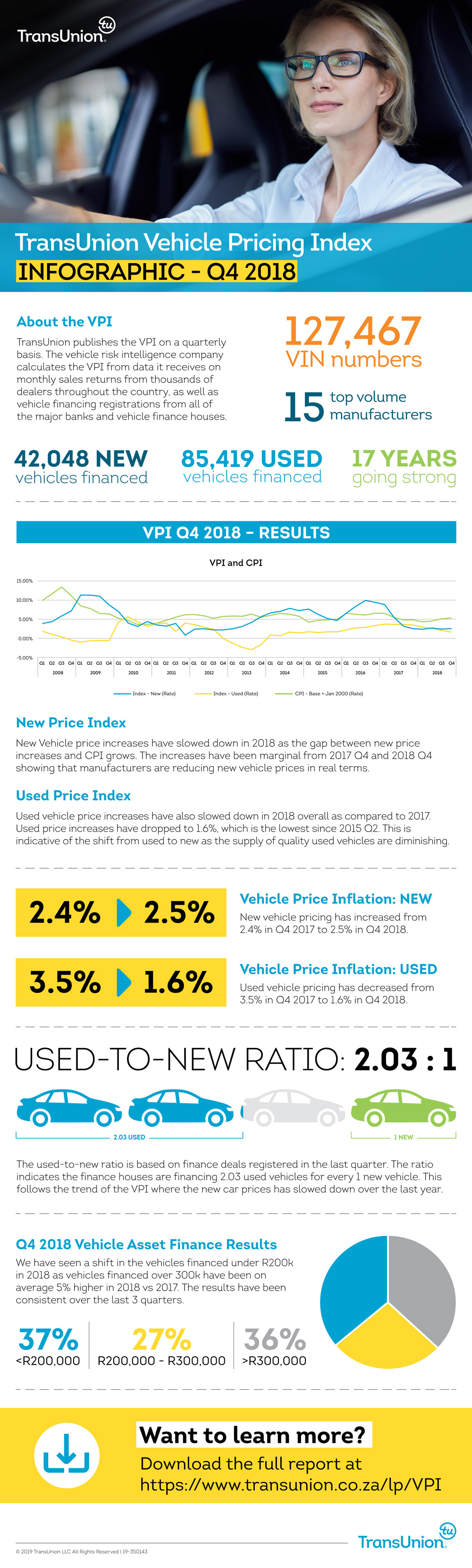

TransUnion Africa’s Vehicle Pricing Index (VPI) was pushed below inflation in the final quarter of 2018 thanks to a constrained economy, a VAT hike and petrol price increases, with the latest data also revealing the percentage of new and used vehicles financed below R200 000 has increased to 37 percent.

The VPI – which measures the relationship between the increase in vehicle pricing for new and used vehicles – fell below inflation for the sixth consecutive quarter, although TransUnion said the outlook for 2019 was “looking more positive”.

New and used vehicle prices showed annual increases of 2,5 percent and 1,6 percent respectively in the fourth quarter of the year. There was a small increase in the rate of growth for new vehicles, which had an annual rate of price inflation of 2,4 percent a year earlier, but a marked decrease in the rate of price inflation for used vehicles, which stood 3,5 percent in Q4 2017.

This was, however, lower than consumer price inflation over the same period, which ended on 4,5 percent in December after a high of 5,2 percent in November 2018.

The VPI report showed the number of new and used vehicles financed below the R200 000 mark stood at 37 percent, up from the previous quarter’s 36 percent. This points to a consistent increase in used car loans, with the average financed deal currently coming in at around R295 000.

For the record, some 27 percent of vehicle finance deals (again, new and used) fell between R200 000 and R300 000, while 36 percent came above R300 000.

“Thirty-nine percent of used vehicle sales during the period were for cars that were less than two years old, while 10 percent were for demo models. In the South African market, there is a significant price differential between new and used vehicles, so demo models and used vehicles less than two years old offer attractive alternatives to purchasing a new vehicle – especially as the baseline price of new vehicles now sits at the R200 000 to R300 000 band,” said Kriben Reddy, head of TransUnion Auto in Africa.

Furthermore, the VPI revealed that new and used passenger vehicle finance deals decreased year-on-year by seven and 15 percent respectively, while the used-to-new ratio decreased from 2,22:1 in Q4 2017 to 2,03:1 in Q4 2018. Total financial agreement volumes in the passenger vehicle market also decreased by 12 percent between Q4 2017 and Q4 2018.

“Challenging economic conditions have seen manufacturers reduce the price of new vehicles in real terms as a way of stimulating sales. It is important to consider the overall cost of owning a vehicle not just the purchase price. Factors such as household disposable income and consumer confidence are also part of the changing dynamics of the vehicle market,” explained Reddy.

He added that low consumer confidence levels had a direct impact on whether a consumer would consider entering into the buying cycle or simply wait for conditions to improve.

“Even when the consumer decides to proceed with a purchase, it is often at a lower price point, which places pressure on manufacturers and dealers and erodes their profit margins.”

After fuel prices surged to record highs in October 2018, consumers saw some relief in January 2019.

“Although further fuel price drops are expected, this is unlikely to have a significant impact on vehicle sales. Aside from the increase in VAT, a depreciating rand and slow economic growth, consumers also face the looming prospect of electricity tariff increases as an embattled Eskom tries to recover,” Reddy added.

He warned that “unless broader economic growth is stimulated”, the automotive sector wouldn’t see a significant improvement in the near term.

“There are only so many levers manufacturers can use to stimulate market demand, including pricing, marketing incentives, trade-in assistance and tools such as residual value that can ease the pressure on consumers’ cash flow. However, measures such as residual value can add up over time and push consumers out of the buying cycle.

“At a dealer level, there are indications that the market is swinging toward used vehicles, which tend to have a larger margin than new vehicle sales. After-sales service is also a potential growth area for dealers and can ease the pressure from lower sales while the market recovers.”

Still, Reddy said there was reason to be optimistic.

“The latest GDP figures show encouraging signs of an economic turnaround, which should translate into improved consumer confidence and better trading conditions. While new vehicle sales are likely to show flat or marginal growth in 2019, there is potential for improved growth in the used car market provided quality stock is available. Dealers will need be cognisant of consumers [who] are struggling with constrained cash flow and indebtedness – offers will need to be tailored accordingly.”

Check out the infographic below…